Economic Injury Disaster Loan Program: Additional Actions Needed to Improve Communication with Applicants and Address Fraud Risks

Fast Facts

To help small businesses affected by COVID-19, the Small Business Administration gave low-interest Economic Injury Disaster Loans and grants to millions of applicants. These funds totaled $224 billion as of February 2021.

But SBA didn't give applicants key information like processing time, loan limits, or status updates—causing confusion and uncertainty for applicants.

Also, the program is susceptible to payment errors. SBA approved at least 3,000 loans worth about $156 million to ineligible applicants. Fraud cases involved, for example, applicants whose businesses did not exist.

We recommended that SBA address these issues.

Highlights

What GAO Found

Economic Injury Disaster Loan (EIDL) applicants and recipients varied in terms of business size, years in operation, and industry, based on GAO's analysis of Small Business Administration (SBA) data from March 2020 through February 2021:

- Business size. A majority of EIDL applicants (about 81 percent) and EIDL recipients (about 86 percent) were smaller businesses (10 or fewer employees).

- Years in operation. A majority of EIDL applicants (about 63 percent) had been in operation for less than 5 years. However, businesses in operation for more than 5 years received the majority of total EIDL loan dollars and had higher approval rates compared to newer businesses.

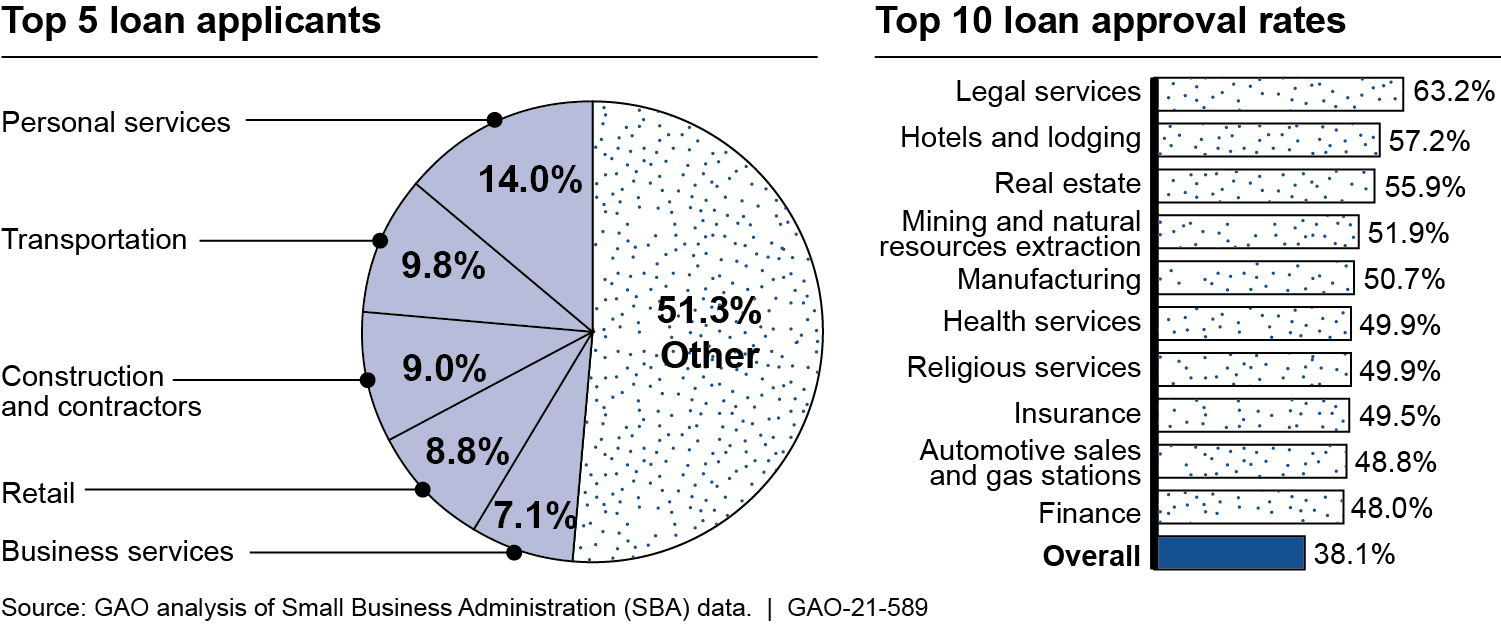

- Industry. Businesses in the personal services and transportation industries made up the largest share of applicants, while those in the legal services and lodging industries were approved for loans at the highest rates (see figure).

Top Loan Applicants and Approval Rates by Business Industry

In addition, small businesses in counties with higher median household income, better internet access, and more diverse populations generally received more loans per 1,000 businesses and larger loans.

EIDL applicants have faced a number of challenges, according to applicants and other business stakeholders GAO interviewed between August 2020 and February 2021. For example, applicants from five discussion groups and several stakeholders cited lack of information and uncertainty about application status as major concerns. In addition, until February 2021, SBA did not provide important information to potential applicants, such as limits on loan amounts and definitions of certain program terms. Lack of important program information and application status put pressure on SBA's resources and negatively affected applicants' experience. For example, SBA's customer service line experienced call surges that resulted in long wait times, and SBA's data showed that 5.3 million applications were duplicates. SBA's planning documents describe in general terms the public outreach to be conducted following disasters, but they do not detail the type or timing of the information to be provided. Developing and implementing a comprehensive communication strategy that includes these details could improve the quality, clarity, and timeliness of information SBA provides to its applicants and resource partners following catastrophic disasters.

GAO's ongoing review of the EIDL program related to COVID-19 has found that the program is susceptible to providing funding to ineligible and fraudulent applicants. For example, as GAO reported in January 2021, SBA had approved at least 3,000 loans totaling about $156 million to businesses that SBA policies state were ineligible for the EIDL program, such as real estate developers and multilevel marketers, as of September 30, 2020. In addition, GAO found that between May and October 2020, over 900 U.S. financial institutions filed more than 20,000 suspicious activity reports related to the EIDL program with the Financial Crimes Enforcement Network. Further, GAO's analysis of 51 Department of Justice cases involving fraud charges for EIDL loans as of March 2021 found that these cases involved identity theft, false attestation, fictitious or inflated employee counts, and misuse of proceeds.

Over the course of its COVID-19 response, SBA has made some changes to address these risks. For example, beginning in June 2020, SBA took actions to improve loan officers' ability to withhold funding for applicants suspected of fraud. However, SBA has not yet implemented recommendations GAO has previously made to address EIDL program risks.

- In January 2021, GAO recommended that SBA conduct data analytics across the EIDL portfolio to detect potentially ineligible and fraudulent applications (GAO-21-265). SBA did not agree or disagree with this recommendation. However, in May 2021, SBA officials stated the agency was in the process of developing analysis to apply certain fraud indicators to all application data.

- In March 2021, GAO recommended that SBA (1) implement a comprehensive oversight plan to identify and respond to risks in the EIDL program, (2) conduct and document a fraud risk assessment, and (3) develop a strategy to address the program’s assessed fraud risks on a continuous basis (GAO-21-387). SBA agreed with all three recommendations. In May 2021, SBA officials stated that the agency had started to assess fraud risk for the program.

Fully implementing these recommendations would help SBA to safeguard billions of dollars of taxpayer funds and improve the operation of the EIDL program.

Why GAO Did This Study

Between March 2020 and February 2021, SBA provided about 3.8 million low-interest EIDL loans and 5.8 million grants (called advances) totaling $224 billion to help small businesses adversely affected by COVID-19. Borrowers can use these low-interest loans and advances to pay for operating and other expenses.

The CARES Act includes a provision for GAO to monitor funds provided for the COVID-19 pandemic. This report examines, among other objectives, the characteristics of program applicants and recipients; the challenges EIDL applicants experienced and the extent to which SBA has addressed them; and the steps SBA has taken to address risks of fraud and provision of funds to ineligible applicants.

GAO reviewed documents from SBA, an EIDL contractor, and two of its subcontractors. In addition, GAO analyzed loan application data, conducted five discussion groups with applicants, and interviewed staff from SBA, six Small Business Development Centers, and six business associations. GAO also analyzed socioeconomic, demographic, and geographic data on EIDL program participants.

Recommendations

GAO recommends that SBA develop a comprehensive communications strategy that includes guidelines for the type and timing of information to be provided to potential and actual applicants of its disaster response programs. SBA agreed with the recommendation.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Small Business Administration |

Priority Rec.

The Associate Administrator of SBA's Office of Disaster Assistance should develop a comprehensive strategy for communicating with potential and actual program applicants in the event of a disaster. Such a strategy should provide guidelines for the types of information and timing of information to be provided to program participants throughout a disaster. The types of information to be addressed in the strategy could include processing steps and time frames applicants might experience through different stages of the loan process. (Recommendation 1) |

SBA agreed with the recommendation and stated that the agency planned to develop a comprehensive strategy for communicating with potential and actual disaster loan applicants, which would include information such as processing steps and corresponding time frames applicants might experience through different stages of the loan process. In December 2024, SBA stated that it was actively developing a robust social media strategy to enhance transparency and communication regarding the various stages of the disaster loan process. SBA stated that the strategy would include detailed messaging that guides disaster survivors from the initial preliminary damage assessment to the transition into long-term recovery. SBA noted that the strategy was not fully complete and that it planned to fully execute the strategy in fiscal year 2025, focusing on recent disasters such as Hurricane Helene and Hurricane Milton. As of March 2025, SBA continues to work on this recommendation.

|