Crypto Investments and Your 401(k)—What’s Being Done to Protect Your Retirement Savings?

A few years ago, some employer-sponsored retirement plans began offering employees the option to invest in crypto assets through their 401(k) plans. Federal regulators and some industry leaders have raised concerns about this investment strategy.

For investors, crypto assets have often been characterized as high-risk, high-reward. Crypto assets have seen record highs in prices, but they have also experienced price crashes, bankruptcies, and fraud concerns.

Today’s WatchBlog post looks at our new report about the prevalence of crypto assets in 401(k) plans and what’s being done to oversee these investments and protect retirement savings.

Image

What do we know about crypto investments in 401(k)s?

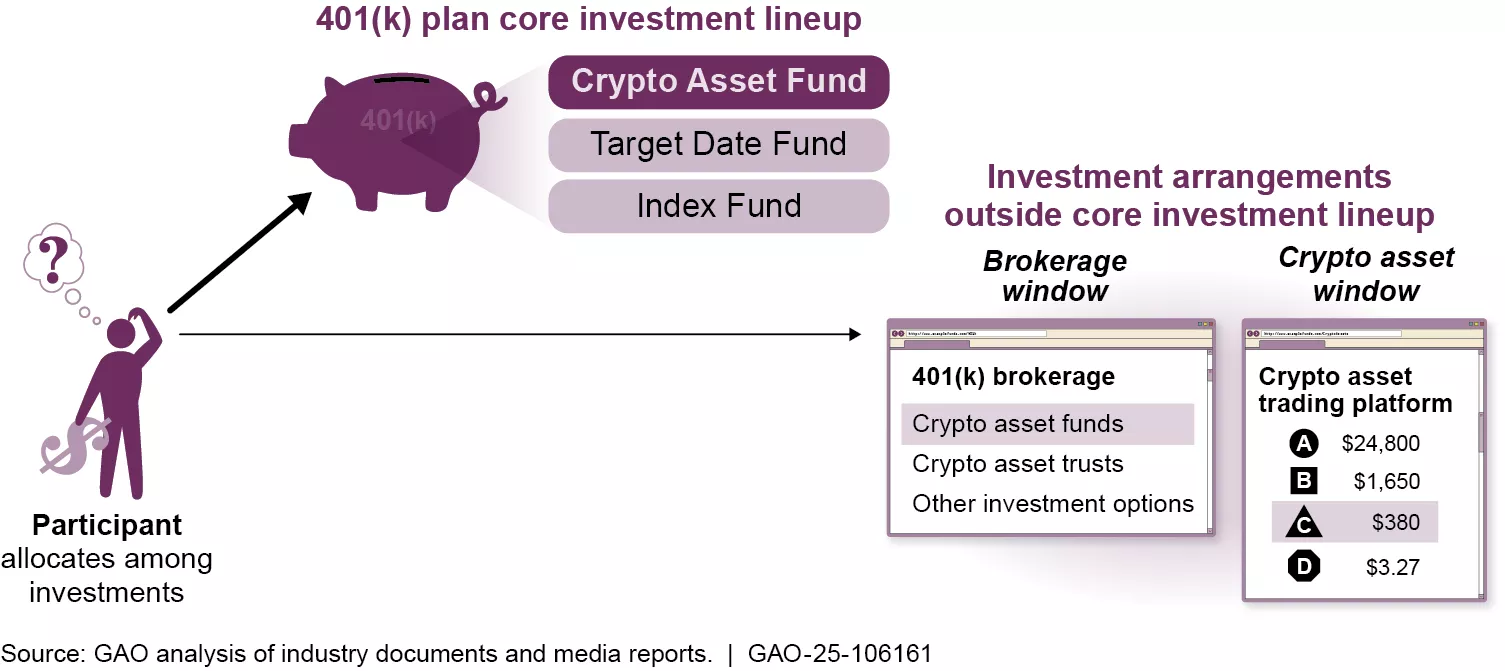

Since 2022, some retirement plans have offered the option to invest in crypto assets through 401(k) plans. Investors may be able to access crypto asset investment options in multiple ways. For example, some may have access to these assets through one of their 401(k) plans’ standard investment options. Or they could access crypto assets outside these options through arrangements that allow them to invest in a wider range of investment options than offered by their plans.

Illustration of 401(k) Plans That Offer Crypto Asset Investment Options

Image

Given their high volatility, choosing crypto assets as an investment option could impact how much money you’re able to secure for retirement. But when we looked at how much participants have invested in crypto assets, we found that important information needed to monitor these investments is not being collected.

The Department of Labor provides oversight and monitoring of employer-sponsored retirement plans to protect against risky investment strategies. To do this, Labor collects data from fiduciaries, such as employers sponsoring 401(k) plans, that are required to act in the best interest of investors. Fiduciaries must report information about investments annually. But we found that this information doesn’t capture the full picture.

For example, Labor does not require fiduciaries to provide detailed data on plans with fewer than 100 participants—meaning some investors are left out of the picture. Even plans with more than 100 participants aggregate some of the investment data they provide Labor—obscuring investments in crypto assets. As a result, Labor can’t measure the prevalence of crypto investments in 401(k) plans or identify plans for investigation to protect investors if needed.

What’s being done to protect investors and their 401(k) investments?

While crypto is a newer investment option, it is regulated by the same long-standing federal regulations that set minimum standards for protecting employees’ retirement plans.

Under the Employee Retirement Income Security Act (ERISA), fiduciaries are required to act in investors’ best interest by considering the risk of loss versus the potential gains of investment strategies. Recently, Labor has cautioned fiduciaries to exercise extreme care before adding a crypto asset option to a 401(k) plan’s core investment lineup.

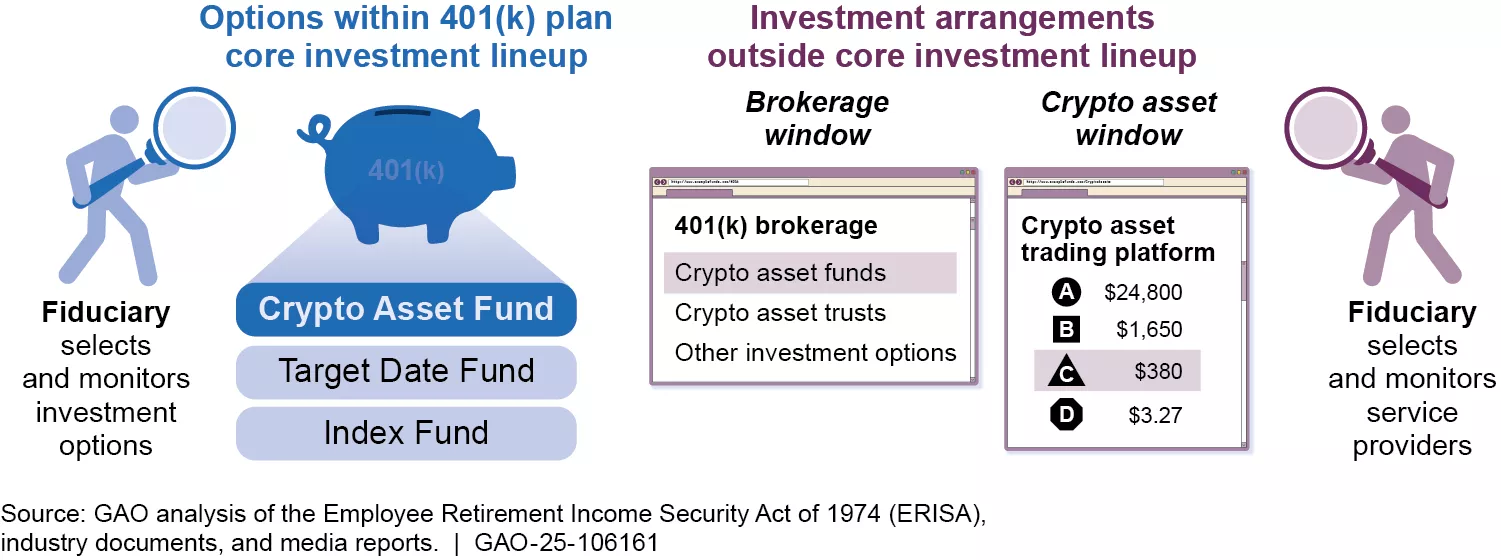

But Labor officials also told us that they generally haven’t required fiduciaries to select and monitor all investment options in accordance with ERISA’s fiduciary standards, such as those offered to participants through self-directed brokerage windows. As a result, participants who invest outside their plans’ options may have to take primary responsibility for monitoring their crypto asset investments.

401(k) Participants May Assume Greater Responsibility When Investing Outside Core Investment Options

Image

What more could be done to improve monitoring of crypto assets?

We have previously cautioned that Labor is not collecting information it needs to fully understand and oversee participant investment in 401(k) plans. In 2014, we reported concerns about the quality and usefulness of the information Labor collects. We recommended ways to improve the information collected. Labor and other agencies have taken steps on our recommendations. But action to address the issues we described above is still needed.

Last year, we also suggested that Congress consider designating a federal regulator to oversee crypto assets. Such oversight could better protect investors from fraud and market manipulation and promote integrity. Legislation aimed at closing regulatory gaps was introduced in the 118th Congress. But none of the bills have become law.

We’ve also recommended that federal agencies, including the Federal Reserve, collectively identify risks posed by crypto assets.

To learn more, be sure to check out our latest report here.

- GAO’s fact-based, nonpartisan information helps Congress and federal agencies improve government. The WatchBlog lets us contextualize GAO’s work a little more for the public. Check out more of our posts at GAO.gov/blog.

- Got a comment, question? Email us at blog@gao.gov.