Tax Enforcement: IRS Audit Processes Can Be Strengthened to Address a Growing Number of Large, Complex Partnerships

Fast Facts

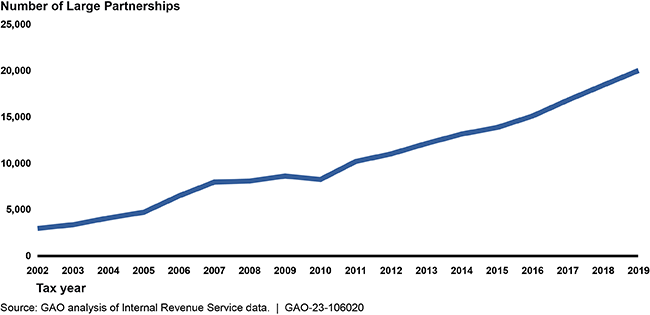

More businesses have been organizing as partnerships. This allows them to pass income and losses to their partners instead of being taxed as corporations. Between 2002 and 2019, the number of large partnerships—with over $100 million in assets and 100 or more partners—increased almost 600%.

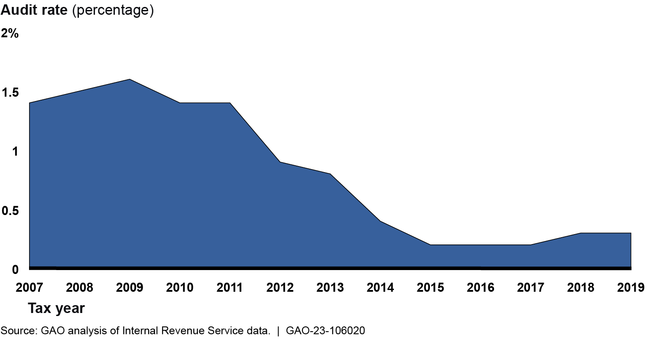

The IRS audit rate for large partnerships has dropped to less than 0.5% since 2007. About 80% of audits conducted don't find tax noncompliance. This may suggest that IRS isn't choosing the riskiest returns to audit or doesn't know how to find noncompliance in these businesses.

Our recommendations would help IRS improve how it selects partnerships to audit.

Large partnerships are increasing in number and complexity, posing tax enforcement challenges.

Highlights

What GAO Found

In tax year 2019, there were 20,052 large partnerships, increasing nearly 600 percent since tax year 2002. Eighty-four percent of large partnerships reported providing finance and insurance services or real estate and rental leasing. Large partnerships can be complex with income or business expenses passing through multiple levels such that a partnership could be a partner in another partnership.

The Internal Revenue Service (IRS) audits few large partnerships—54 in tax year 2019—and the audit rate has declined since 2007. More than 80 percent of the audits resulted in no change to the return on average from tax years 2010 to 2018, double the rate of large corporate audits. For those that did change, the average adjustment was negative $264,000. IRS officials attributed the declining audit rate to resource constraints. The Inflation Reduction Act of 2022 (IRA) provided IRS with $45.6 billion for enforcement activities through the end of fiscal year 2031, and in response IRS identified large partnerships as an enforcement priority. About $1.4 billion of this funding was rescinded in 2023 with a White House briefing reporting an agreement to reduce future funding by $20 billion.

Audit Rate for Large Partnerships, 2007–2019

As part of its audit selection process, IRS uses statistical models to help review partnership returns for potential noncompliance, but the models were developed without using representative samples of returns and with untested assumptions. Additionally, IRS has not developed a plan to incorporate feedback from audit results into the models. Addressing these modeling issues could improve IRS's ability to better identify and audit noncompliant partnerships.

IRS planning documents state that it will expand enforcement efforts related to large, complex partnerships using IRA funding. However, IRS has not defined complexity or size in terms specific enough to guide enforcement efforts. IRS also has not developed measures to ensure that additional audits focus on these entities. Developing such a definition and specific outcome measures would help IRS develop plans, track resources used, and assess the results of these new investments in large partnership audits.

Why GAO Did This Study

Business activity has increasingly shifted toward legal structures known as partnerships and away from C corporations subject to the corporate income tax. A partnership is generally an unincorporated organization with two or more members that conducts a business and divides profits. Partnerships usually do not pay income taxes as entities but pass the net income or losses to partners, such as individuals or corporations, who then report the income and pay any applicable taxes.

GAO was asked to examine trends in large partnerships and IRS auditing of them. This report (1) summarizes the number and characteristics of large partnerships; (2) describes the resources used and results of audits of large partnerships; and (3) assesses IRS's efforts to identify potential noncompliance risks in large partnerships. For purposes of this report, large partnerships are defined as having $100 million or more in assets and 100 or more total partners.

GAO analyzed IRS data pertaining to business and audit activity for tax years 2002 through 2019, the most recent year for which complete data were available; compared IRS statistical models to relevant statistical modeling standards; interviewed agency officials; and held discussion groups with IRS staff.

Recommendations

GAO is making four recommendations to IRS, including improving the design of its models as well as developing guidance to define and measures to track large and complex partnership audits. IRS agreed with GAO's recommendations.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Internal Revenue Service | The Commissioner of Internal Revenue should use representative sampling of partnership returns, including those on which IRS's current partnership models do not identify risk factors, to help identify additional noncompliance that may not be detected and to improve the agency's understanding of the models' effectiveness. (Recommendation 1) |

IRS agreed with the recommendation. In January 2024, officials described a plan to test statistical models used to identify potential noncompliance risks among the largest partnerships by September 30, 2024. As part of this plan, officials said subject matter experts will review a sample of large partnership returns selected from all categories of identified risk. This is intended to improve the statistical models' ability to identify potential noncompliance. We will continue to monitor IRS's efforts to address our recommendation.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should test and validate the key assumptions used in IRS's partnership models through analysis of data on audit outcomes or other research and develop a formal process for using audit results and other data as they become available to improve model performance. (Recommendation 2) |

IRS agreed with the recommendation. In January 2024, IRS officials described plans to gather and utilize feedback throughout the examination process to improve modeling efforts. We will continue to monitor IRS's efforts to address our recommendation.

|

| Internal Revenue Service |

Priority Rec.

The Commissioner of Internal Revenue should develop guidance defining large, complex partnerships and the characteristics of those entities. (Recommendation 3) |

IRS agreed with the recommendation. In April 2024, officials reported they are working with IRS research officials to understand the partnership population and identify more specific segments of partnerships. In July 2024, IRS officials reported that they anticipate addressing this recommendation by September 30, 2024. To fully implement this recommendation, IRS will also need to develop guidance based on the characteristics of the large partnership population it identifies as an enforcement priority. Doing so will better inform management by tracking audit resources used and results and help IRS better focus on the cases that will help it achieve its goals.

|

| Internal Revenue Service |

Priority Rec.

The Commissioner of Internal Revenue should identify and implement measures for tracking progress toward agency objectives that reflect the definitions and guidance for large, complex partnerships, which should include creating additional activity codes for IRS to track audit resources used and results. (Recommendation 4) |

IRS partially agreed with this recommendation. IRS officials reported in April 2024 that they do not agree that creating additional activity codes is necessary. They believe that the agency's existing codes are sufficient to track staffing and audit results of partnership compliance efforts. In its May 2024 annual update to its Strategic Operating Plan, IRS stated that it plans to increase audit rates for partnerships with $10 million or more in assets from 0.1 percent in tax year 2019 to 1 percent in tax year 2026 using IRA funds. However, we found that IRS's existing activity codes for partnership audits are not based on the assets partnerships hold and instead based on overly broad categories of how many taxpayers are members of the partnerships. Without activity codes organized by asset size similar to those for large corporate audits, it will be difficult to track progress for the planned goal. To fully implement this recommendation, IRS needs to create measures and activity codes that align with its current focus on large, complex partnerships as part of the Strategic Operating Plan. Doing so will allow IRS to identify these entities and track progress towards the agency objective of increasing enforcement activities of large, complex partnerships.

|