Tax Equity: Lack of Data Limits Ability to Analyze Effects of Tax Policies on Households by Demographic Characteristics

Fast Facts

The federal government considers how tax policies affect taxpayers at various income levels—but knows little about how they affect taxpayers across other demographic characteristics (such as race, ethnicity, and sex).

The IRS doesn't collect such information about taxpayers, but other agencies (like the Census Bureau) do. However, there are legal restrictions on sharing such data among agencies.

We recommended that Congress consider revising relevant laws to facilitate secure interagency data sharing. Doing so could help policymakers analyze the effects of tax policies on different types of households.

Highlights

What GAO Found

GAO found that tax data are not consistently linked to households' demographic information. The Internal Revenue Service (IRS) collects demographic data that are explicitly referenced in the tax code. According to the Department of the Treasury, IRS cannot collect demographic data under current law unless such data are necessary for administering the tax code. As a result, analysts have limited ability to assess the effects of tax laws, including COVID-19-related tax relief provisions, by demographics such as households' race, ethnicity, and sex.

Legal restrictions on interagency data sharing limit agencies' ability to analyze how the tax system interacts with households by demographic characteristics. Several entities, such as the Office of Management and Budget, have emphasized the importance of collecting and sharing demographic data for policy evaluation. Entities also highlight the importance of protecting the privacy and security of those data. GAO identified options for consistently producing linked taxpayer and demographic data, such as surveys and interagency data matching. Another option is to impute the demographic information of taxpayers. Treasury is developing an imputation method. While Treasury is evaluating the reliability and limitations of imputation, it has not evaluated the feasibility of other options to produce data that would support more reliable analyses.

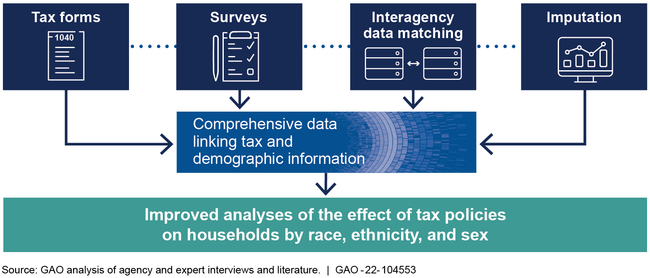

If tax data could be linked to households' demographic data in a way that still protects the privacy and security of those data, policymakers and researchers would have better tools for consistently and systematically analyzing the relationship between tax policies and household demographics (see figure).

Examples of Options for Data Collection and Analysis

In the absence of linked taxpayer and demographic data, GAO used a model that simulated the tax outcomes of households based on 2017 Census Bureau survey data. For most of the provisions examined, GAO estimated disparities in tax outcomes across households based on race, ethnicity, or sex. For example, there were differences by race in estimated eligibility of use and average dollar amount of the child tax credit. These disparities generally remained after GAO controlled for some variation in income—using income quintiles—indicating potential inequalities beyond those based on income.

Why GAO Did This Study

The U.S. has a large and increasing gap in income and wealth by race, ethnicity, and sex. However, little is known about the effects of tax policies across demographic characteristics. The tax code does not tax individuals differentially based on certain demographics. However, some researchers have noted how it could result in potential unintended disparate tax outcomes.

The CARES Act includes a provision for GAO to report on its ongoing COVID-19 monitoring and oversight efforts. GAO was also asked to review how selected tax policies affected households by race, ethnicity, and sex as part of this oversight.

This report (1) examines approaches for analyzing the effect of tax policies, including some in the CARES Act and related legislation, on households by race, ethnicity, and sex, and (2) estimates how households use selected tax provisions by race, ethnicity, and sex. GAO interviewed 21 experts and reviewed literature on tax policy and demographics. GAO also used Census data to estimate households' use of tax provisions.

Recommendations

GAO is making one matter for congressional consideration to revise relevant laws to facilitate interagency data sharing. GAO also recommends that Treasury evaluate the feasibility of other options to produce secure, linked taxpayer and demographic data. Treasury stated it is focusing on imputation and has considered other options. Moving forward, evaluating other options would enhance Treasury's efforts to produce such data.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| Congress should consider revising relevant laws, such as those in Titles 13 and 26, as appropriate, to facilitate interagency data sharing that would allow for more accurate, consistent, and systematic analyses of any effects of existing and proposed tax policies in relation to taxpayers' demographics in a secure manner that protects the confidentiality of those data. (Matter for Consideration 1) | As of March 2024, Congress has taken no action on this matter. |

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of the Treasury | The Secretary of the Treasury, as part of the department's work on equity analysis of tax policy, should evaluate the feasibility of alternative methods, such as interagency data sharing or surveys, for producing secure, linked taxpayer and demographic data. (Recommendation 1) |

Treasury neither agreed nor disagreed with the recommendation and said it is focusing its current efforts on developing an imputation method. Treasury agreed with GAO on the importance of understanding the effects of tax policies by demographic characteristics and in May 2023 released a report on how the disbursement of the First Round Economic Impact Payments varied by race/ethnicity, age, sex, income, and household composition using interagency data sharing. Previously, in January 2023, Treasury had also released a report examining tax expenditures by race and ethnicity using imputation methods. However, as of March 2024 Treasury had not indicated how it plans to evaluate the feasibility of alternative methods or if it plans to rely on interagency data sharing or imputation methods to evaluate the effects of other tax policies by demographics. We continue to monitor what actions the agency has taken in response to this recommendation.

|