DOD Financial Management: Improvements Needed in Army's Efforts to Ensure the Reliability of Its Statement of Budgetary Resources

Highlights

What GAO Found

The Army has made important progress in developing its financial improvement plan (FIP) for budget execution to help guide its General Fund Statement of Budgetary Resources (SBR) audit readiness efforts. This FIP covers current year activity associated with the recently deployed General Fund Enterprise Business System (GFEBS) emphasizing the implementation of effective business processes. However, the Army did not fully complete certain tasks in accordance with the Financial Improvement and Audit Readiness (FIAR) Guidance to ensure that its FIP adequately considered the scope of efforts required for audit readiness. For example, the Army did not consider the risks associated with excluding current year activity associated with legacy systems and did not adequately identify significant SBR activity attributable to service provider business processes and systems. These activities may continue to represent material portions of future SBRs and, if not auditable, will likely affect the Army's ability to achieve audit readiness goals as planned.

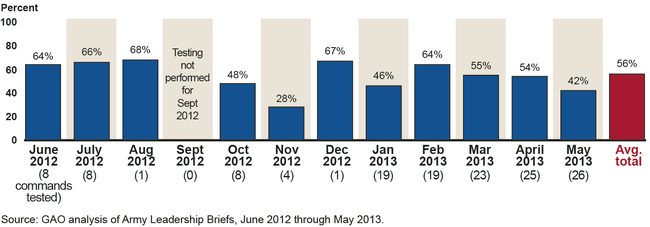

For GFEBS-related audit readiness activities within the scope of its FIP for budget execution, the Army documented controls in narratives and flowcharts and performed monthly tests to assess their effectiveness. Based on test results from June 2012 through May 2013, the Army identified extensive deficiencies, such as lack of appropriate reviews or approvals, and had an average failure rate of 56 percent.

Army's Reported SBR Internal Control Test Failure Rates for Commands Tested

The Army did not fully follow the FIAR Guidance in performing the tasks required. For example, the Army's documentation and assessment of controls were not always complete or accurate. Further, extensive deficiencies identified by Army had not been remediated prior to an independent public accountant's (IPA) examination of its audit readiness efforts.

Overall, the gaps and deficiencies identified above are largely due to the Army's focus on (1) the audit readiness of new GFEBS processes despite continued reliance on legacy systems and service providers and (2) asserting audit readiness before correcting extensive control deficiencies. Army officials cited adherence to assertion and IPA examination milestones as essential. However, this approach raises serious concerns regarding the likelihood that SBR audit readiness will occur as planned and the Army's ability to ensure the accuracy of financial information used to monitor budgetary resources to achieve its mission.

Why GAO Did This Study

The National Defense Authorization Act for Fiscal Year 2013 requires the Department of Defense (DOD) to describe how its SBR will be validated as ready for audit by September 30, 2014. The DOD Comptroller issued the FIAR Guidance to provide a standard methodology for DOD components to use to develop and implement FIPs, improve financial management, and achieve audit readiness. The Army's FIP for budget execution provides a framework for planning, executing, and tracking essential steps with supporting documentation to achieve audit readiness of its General Fund SBR.

GAO is mandated to audit the U.S. government's consolidated financial statements, including activities of executive branch agencies such as DOD. This report identifies the extent to which the Army developed and implemented its General Fund SBR FIP for budget execution in accordance with the FIAR Guidance with regard to (1) determining the scope of activities included in the FIP and (2) completing those activities included in the scope of the FIP. GAO reviewed the Army's FIP to determine whether it contained the elements required by the FIAR Guidance and reviewed test results, status reports, and other deliverables.

Recommendations

GAO recommends that among other things, the Army take steps to improve implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and ensure that all significant SBR processes, systems, and risks are adequately considered and identified deficiencies are resolved. The Army concurred with GAO's recommendations.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should identify activity attributable to assessable units associated with service provider systems and business processes having a significant impact on the Army's SBR. |

The Army concurred with this recommendation. In March 2015, Army officials indicated that the Army leveraged object class codes in its enterprise resource planning (ERP) systems to stratify business processes that have a significant impact on the Schedule of Budgetary Activity for fiscal year 2015 activity. The Army provided documentation supporting this effort; however, the documentation did not identify all activity attributable to assessable units associated with service provider systems and business processes having a significant impact on the Army's Statement of Budgetary Resources. In September 2017, Army officials stated that they were in the process of refining data categorization that links Army and Service Provider activity to business processes, assessable units, and systems. In July 2018, Army provided activity for the first eight months of fiscal year 2018 attributable to assessable units associated with service provider systems. Army's identification of activity and association of that activity to assessable units should facilitate Army's efforts achieve an auditable SBR. In August 2019, Army provided a reconciliation of Obligations Paid by significant business process for the first ten months of fiscal year 2019. Army attributed over 99 percent of outlay transactions to business processes having a significant impact on the Army's SBR. The Army's identification of outlay transactions by business processes should improve their audit readiness and compliance with FIAR Guidance.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should coordinate efforts with service providers to obtain and document within memorandum of understanding memorandums of understanding a shared understanding of roles and responsibilities for processing Army data. |

The Army concurred with this recommendation. The Army established a Mission Work Agreement (MWA) with Defense Finance and Accounting Service (DFAS), its most significant service provider, and documented concept of operations (CONOPS) regarding various business processes, such as civilian pay and Fund Balance with Treasury. However, the MWA and CONOPS did not include sufficient detail required to adequately understand roles and responsibilities for processing and reporting the Army's financial data. In January 2016, the Army indicated that it was developing a corrective action plan to formalize policies, procedures, and processes to assess third party providers that host or manage the Army's financial systems and data and will use this assessment to clarify its understanding of shared roles and responsibilities for processing Army data. In July 2018, Army provided copies of MOUs with 15 of its relevant service providers. Army's implementation of this recommendation should facilitate efforts to achieve financial statement auditability.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should identify and document qualitative risks and other factors, including those associated with the Army's reliance on service provider readiness efforts as well as other processes and systems supporting significant portions of its SBR that the Army excluded from the scope of its readiness efforts and assess their potential impact on SBA and full SBR auditability and established timelines required to effectively achieve audit readiness. |

The Army concurred with this recommendation. In the May 2015 Financial Improvement Audit Readiness (FIAR) Plan Status Report, the Army identified qualitative risks and other factors related to its reliance on service providers and processes and systems excluded from the scope of its readiness efforts. For example, the Army identified risks related to the ability of the Defense Finance and Accounting Service to ensure that journal vouchers are fully supported and documented. Additionally, in its assessment of financial reporting risks and major processes, the Army assessed the complexity and other factors associated with beginning balances which had been excluded from the scope of its readiness efforts. Further, the Army included its assessment of legacy systems in the May 2015 FIAR Plan Status Report. The Army reported that it is still relying on legacy systems to support business processes and operations and that replacing these systems is critical to being audit ready in fiscal year 2017. Army's actions have addressed the intent of this recommendation.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should update the Army's determination for achieving SBR audit readiness included in DOD's FIAR Plan Status Report to address NDAA requirements. |

The Army concurred with this recommendation. In the May 2015 FIAR Plan Status Report, the Army updated its determination that it would achieve Statement of Budgetary Resources (SBR) audit readiness by September 30, 2017. As a result, the Army complied with National Defense Authorization Act (NDAA) requirements.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should completely and accurately document the linkage of financial reporting objectives to control activities. |

The Army concurred with this recommendation. In June 2015, Army officials indicated that the Army's four financial reporting objectives had not yet been linked to control activities. Army officials stated that the Army was continuing to analyze collection, disbursement, and Fund Balance with Treasury processes and anticipated linking these financial reporting objectives to control activities based on these efforts. The Army's Control Catalogue as of May 2017, documented certain financial reporting objectives and linked them to control activities. However, as of July 2018, Army linked control activities to only 6 of the 13 financial reporting objectives noted during our audit. For fiscal year 2019, the services are now under audit and have been receiving findings and recommendations from auditors. Our recommendation was based on steps in DOD's Financial Improvement and Audit Readiness (FIAR) Guidance, which has been retired. However, for the audit, Army created Risk and Control Matrices and is in the process of linking key controls to 15 central processes they identified. As of September 2019, Army linked key controls to 1 of the 15 central processes. In February 2020, an Army official indicated that they had completed a second Risk and Control Matrix and expected another 10 to be complete by October 2020. The planned population of Risk and Control Matrices go beyond our recommendation which was related to the FIAR guidance. Given the age of this recommendation, the retirement of the FIAR Guidance, and ongoing audit efforts at the Army, we are closing this recommendation as not implemented.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should document criteria and processes for identifying key information technology systems that have a significant impact on the Army's SBR audit readiness. |

The Army concurred with this recommendation. In March 2015, Army officials indicated that the Army was in the process of identifying IT systems with a significant impact on the Army's Statement of Budgetary Resources (SBR) audit readiness. Army officials also stated that for the fiscal year 2015 Schedule of Budgetary Activity Audit, the independent public accountant was conducting walkthroughs and assessing information technology systems for significant impact on Army's SBR audit readiness. Army provided a ten page list of systems they identified as key but did not provide the criteria used to identify the key systems. Subsequently, we requested the criteria used to identify the key systems. In July 2018, the Army provided a reduced list of 49 key systems, but did not explain the criteria used to identify the key systems. In August 2019, Army provided the criteria and processes used to identify key information technology systems and a list of the systems considered key to audit readiness. The Army's establishment of criteria and processes used to identify key information technology systems should improve their audit readiness and compliance with FIAR Guidance.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should obtain and assess the results of service provider SSAE No. 16 examinations upon completion to determine the adequacy of internal controls and document complete end-to-end business processes. |

The Army concurred with this recommendation. As of January 2016, Army officials indicated that the Army continued to assess SSAE 16 reports including complimentary controls and incorporating end-to-end business processes as applicable. As of September 2017, the Army was still in the process of obtaining the SSAE 18 reports and conducting the assessments. In July 2018, Army provided its evaluations for 15 completed Service Organization Control Reports. Army's implementation of this recommendation should facilitate efforts to achieve financial statement auditability.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should update the Army's FIP status reports to include actions to address identified deficiencies related to service providers, systems, and other known issues, along with an assessment of their severity, including references to current control activities with accurate estimates of the completion status. |

In March 2015, Army officials provided documentation indicating that the Army included actions to address identified deficiencies along with its assessment of their severity, including references to applicable control activities with estimated completion dates in its corrective action plans. In DOD's November 2016 FIAR Plan Status report, Army included a table on Material Weaknesses, and Notices of Findings and Recommendations. The table includes corrective actions and completion dates. In addition, in January 2017, Army provided additional detail support for the table included in the November 2016 FIAR Plan Status Report.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should link corrective actions and estimates for their completion in FIP status reports to (1) specific CAP tasks to resolve deficiencies and their underlying causes and (2) dates for their expected completion. |

In March 2015, Army officials indicated that the Army developed corrective action plans and were in the process of implementing them. In DOD's November 2016 FIAR Plan Status report, Army included a table on Material Weaknesses, and Notices of Findings and Recommendations. The table included corrective actions and completion dates. These actions sufficiently addressed this recommendation.

|

| Office of the Assistant Secretary for Financial Management and Comptroller | To improve the Army's implementation of the FIAR Guidance for its General Fund SBR FIP for budget execution and facilitate remaining efforts to achieve SBR auditability, the Assistant Secretary of the Army, Financial Management and Comptroller should correct significant deficiencies or material weaknesses identified before asserting audit readiness and engaging an IPA to validate the assertion. |

The Army concurred with this recommendation. In March 2015, Army officials indicated that the Army was working to resolve identified significant deficiencies and material weaknesses. In January 2016, Army officials indicated that the Army was assessing findings from an Independent Public Accountant (IPA) in connection with its audit of Army's fiscal year 2015 Schedule of Budgetary Activity to identify deficiencies identified during previous audit readiness efforts. Repeat findings were incorporated into corrective action plans. In September 2017, Army indicated that correcting deficiencies is an ongoing process and does not preclude Army from asserting audit readiness. Since DOD hired an IPA to conduct an audit for fiscal year 2018, we are closing this recommendation as not implemented.

|