When the Student Loan Payment Pause Ended, Did Borrowers Pay?

Student debt is one of the fastest-growing forms of household debt. More than 43 million people had federal student loans, totaling about $1.5 trillion at the start of 2024.

During COVID-19, student loan borrowers received a reprieve when payments on their loans were paused for more than 3 years. But when payments restarted in October 2023, there was concern about potentially high rates of delinquency after such a prolonged period of postponed payments.

So, what happened when payments came due? Today’s WatchBlog post looks at our new report for Congress about what happened when the student loan payment pause ended.

Image

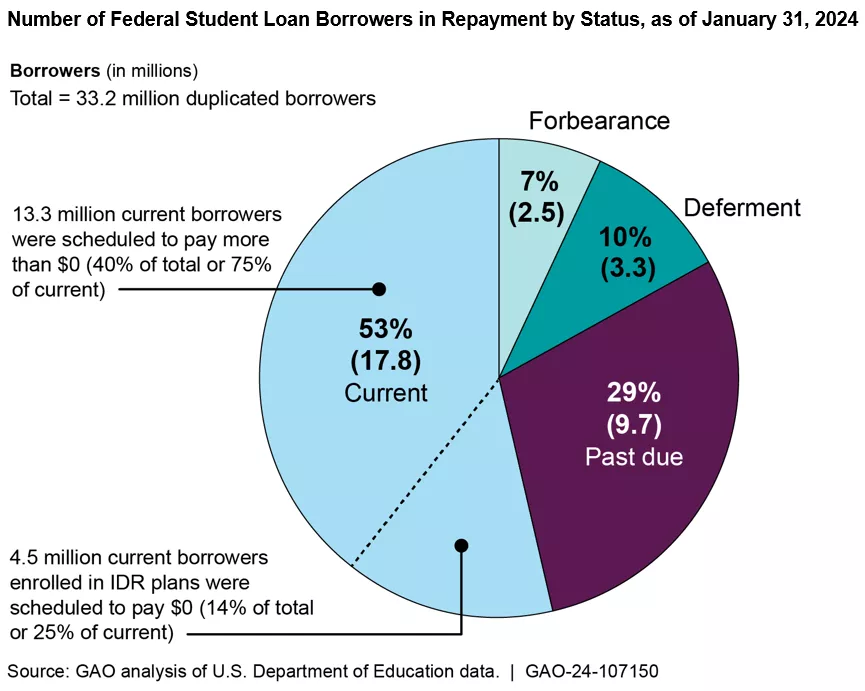

Many borrowers did not begin to pay when the pause ended

In our new report, we looked at the status of federal student loans as of January 2024—just a few months after the payment pause ended and loans came due.

Current on payments. About 17.8 million borrowers were in good standing on their loans. About 4.5 million of the borrowers in good standing had scheduled payments of $0 on income-driven repayment plans. These plans base monthly payments on a borrower’s income and family size and offer forgiveness of any remaining loan balance at the end of the repayment period. Monthly payments can be as low as $0 for some borrowers and still count toward forgiveness.

Past-due on payments. Nearly 10 million borrowers were past due on their loan payments as of January 31. The Department of Education typically reports borrowers as delinquent to credit reporting agencies when they become 90 days past due on their loans. But the department is forgoing this practice as part of its temporary relief program known as the “on ramp.” As of January 31, Education reported that nearly 6.7 million borrowers had been shielded from negative credit reporting since monthly payments resumed.

In forbearance or deferment. Another about 6 million borrowers did not need to make payment on their loans. About 2.5 million borrowers were in forbearance—a status that allows borrowers experiencing financial struggles to temporarily postpone or reduce monthly payments. About 3.3 million borrowers were in deferment, which allows borrowers to temporarily postpone payments if they are returning to school, in active-duty military service, unemployed, or experiencing economic hardship.

Image

Temporary relief programs and repayment plans offered

When the payment pause ended, Education established temporary relief options for some borrowers to help them resume payments. As discussed above, some borrowers were shielded from negative credit reporting through the “on ramp.” Education also implemented Fresh Start, which allows borrowers to more easily restore defaulted loans to good standing. Borrowers with defaulted loans can learn more about Fresh Start on Education’s website. Both Fresh Start and the “on-ramp” are scheduled to end September 30.

Repayment plans. Should borrowers need help making payments, Education offers four income-driven repayment plans. As of January, the most popular plan was the newest option—Saving on a Valuable Education (SAVE). About 25% of borrowers were enrolled in SAVE.

In July, a federal appeals court granted an emergency motion for a stay that temporarily prohibits Education from implementing the SAVE plan. Since then, Education announced that borrowers enrolled in the SAVE plan would be placed in an interest-free forbearance while litigation was ongoing.

What are the repayment plans? The differences between the four plans include the percentage and definition of income used to calculate monthly payments amounts and the years required for repayment.

- Saving on a Valuable Education (SAVE)—This plan requires payments that are generally 10% of your discretionary income. The remaining unpaid balance of loans is forgiven up to 20 or 25 years. The SAVE plan generally offers borrowers lower payments because Education sets its payments based on a smaller portion of borrowers’ income than other plans. Also, borrowers who make a full monthly payment are not charged any remaining accrued interest that month.

- Income-Contingent Repayment (ICR)—Payments are 20% of your discretionary income or what you would pay on a repayment plan with a fixed payment over the course of 12 years, adjusted according to your income. The remaining unpaid balance of loans is forgiven after 25 years.

- Income-Based Repayment (IBR)—Depending on when you first took out loans (before or on or after July 1, 2014), payments are generally 10% or 15% of the borrower’s discretionary income, but never more than the 10-year Standard repayment plan amount. The remaining unpaid balance of loans is forgiven after 20 or 25 years.

- Pay As You Earn (PAYE)—Payments are generally 10% of your discretionary income, but never more than the 10-year Standard repayment plan amount. The remaining unpaid balance of loans is forgiven after 20 years.

You can find out more about which plan is the best fit for you and how to apply for a plan by visiting Education’s website.

Learn more about our work on student loans by checking out our latest report.

- GAO’s fact-based, nonpartisan information helps Congress and federal agencies improve government. The WatchBlog lets us contextualize GAO’s work a little more for the public. Check out more of our posts at GAO.gov/blog.

GAO Contacts

Related Products

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.